Europe's online source of news, data & analysis for professionals involved in packaged media and new delivery technologies

ANALYSIS: Transactional TV-based Video-on-Demand on the rise

One of the advantages of transactional TV-based Video on Demand is that video content is delivered via a closed digital platform, capturing almost 100% legitimate consumption and spending, points out TANIA LOEFFLER, Video Analyst with IHS. TV-based VOD also enters into households via set-top boxes, already attached to the device on which most people still want to watch the majority of their movie content - their television.

Given current movie windowing structures, movie content on TV-based VOD services has traditionally been 'fresher' in comparison to over-the-top (OTT) digital or 'online' movie services. Frequently, TV-based VOD providers also create a trusted content ecosystem which will include free TV catch-up services and automated billing for transactions - all at the touch of a remote control. Key to capturing legitimate spending and growing consumption is that TV-based VOD offers consumers an ease of use which works to streamline uptake friction, quickly establishing the platform in new homes.

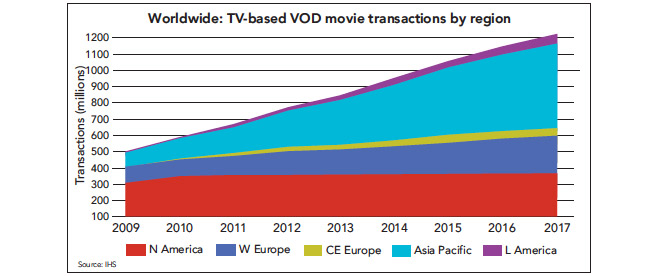

As a result of significant advantages, of the three transactional digital distribution channels, TV-based TVOD has pulled away by a significant margin in terms of generating recorded movie transactions. In 2009, TV-based TVOD accounted for 510 million or 4% of total worldwide movie transactions, doubling to 8% in 2013; forecast to reach 1.2 billion transactions by 2017 or an 11% share. In contrast, over-the-top (OTT) digital retail and rental movie transactions combined are only forecast to account for a share of 5% of worldwide movie transactions by 2017.

As they operate over the open internet, OTT movie services are forced to directly compete with piracy and face significantly stronger competition from online-based subscription services, such as Netflix, which have been very efficient at making their movie services available across most devices connectable to the television set.

Households with access to a TV-based VOD platform or 'on-demand-enabled' households, are defined as homes with push-VOD, near-VOD (nVOD) or VOD capability. In many markets, homes may have access to multiple VOD platforms via their television provider, creating an overlap for penetration. The kind of VOD platform available to consumers depends on the sophistication of the network 'backbone' that provides a given region with its television services, with there often being significant differences in technical development between countries in the same region, or even within countries themselves.

Push-VOD involves a limited amount of content being pushed out and stored locally on individual STBs for a limited amount of time; but, this content can be consumed exactly at a time of the consumer's choosing. The nVOD platform provides a sequence of linear channels where content is staggered, which provides for more content than push-VOD, but consumers are forced to watch movies in pre-scheduled time-slots and content is not available indefinitely. Content is limited by cost as nVOD requires a channel's worth of bandwidth per timeslot.

True-VOD, just referred to as VOD, is considered the most advanced platform. It technically supports a much greater scope of content, with extensive back catalogues made available indefinitely and permits consumers to watch whatever they want, whenever they want. It requires the connection between the VOD provider and the households to have an advanced degree of technical development, and is therefore more commonplace in more mature TV markets such as North America and Western Europe. Although growth for push-VOD and nVOD households does make a positive impact on consumption, it is VOD, with a combination of deep content range and constant availability at a click of a button, which accelerates movie consumption.

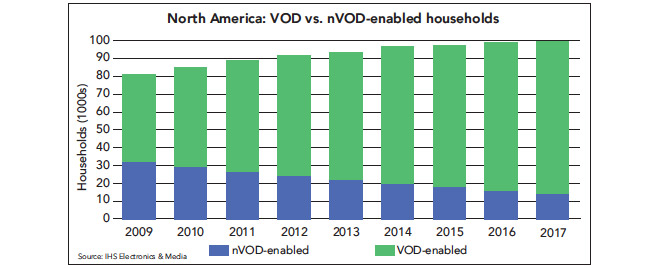

North America is the most mature market for transactional TV-based VOD, both in terms of the penetration for on-demand enabled households and the depth of services available to consumers. In 2013, 70% of households in North America were nVOD and/or VOD enabled; when push-VOD is included, household penetration increases to 76%.

However, the US has largely reached a saturation point for pay TV subscribers, with North America the only region where pay TV penetration is set to decline over the forecast period (2013-2017). Unlike in many less mature movie markets, where TV-based TVOD as a platform is still developing, any year-on-year growth for TV-based VOD movie transactions is no longer directly linked to new homes becoming on?demand-enabled in North America.

The number of VOD homes in North America is set to increase by an average of 4.6% between 2013 and 2017, reaching an installed base of 85, 974 by 2017. However, the number of nVOD and push-VOD homes will decrease, resulting in penetration remaining consistent. During this same time period, TVOD movie transactions are forecast to remain flat in the region at (-0.1% CAGR) at 357 million by 2017.

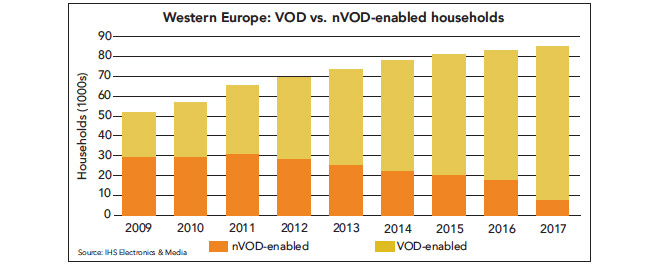

In contrast, Western Europe has seen stronger growth for TV-based TVOD movie transactions - from 100 million in 2009 to 162 million recorded in 2013 - an average yearly increase of 13%. This growth in consumption was the result of the rollout of new VOD-enabled households and offerings across the region. The number of VOD-enabled homes in Western Europe increased by a yearly average of 20.4% between 2009 and 2013. The installed base for nVOD homes, however, decreased by an average of 3.5% over the same time period as TV households were digitized or upgraded from nVOD to VOD platforms.

The total number of VOD/nVOD enabled households in the region is forecast to increase 3.6% every year between 2013 and 2017, reaching 84,926 by the end of the forecast period. Growth for movie VOD transactions is also forecast to continue, although will slow to an average annual increase of 9%, reaching 232 million transactions by 2017.

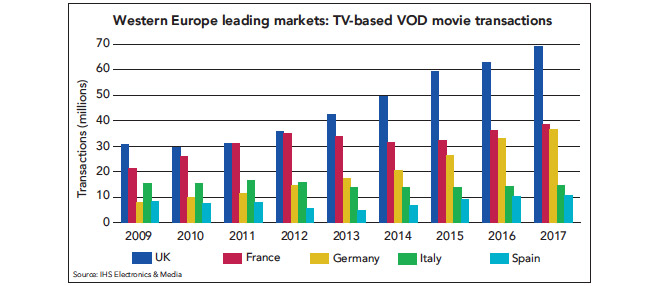

In terms of transactions, the UK remains Western Europe's largest TV-based VOD market, generating 41.7 million TV-based VOD movie transactions in 2013, forecast to increase 68.5 million by 2017, by when the UK will account for a 29% share of all TV-based VOD movie transactions generated in Western Europe.

However, growth is not even among all countries in the region. At 22,352 VOD/nVOD households, France has the largest installed base for TV-based VOD in 2013. But in terms of TV-based VOD movie transactions, French volumes actually declined, from 34.8 million in 2012 down to 33.7 million in 2013. Consumption is forecast to drop further to 31.1 million by year-end 2014.

Careful management in terms of price and depth of offering is a key to ensure continued uptake of transactional movie consumption via TV-based VOD platforms in any region. Despite being a digital platform and having exhibited year-on-year growth for a much extended period of time, TV-based VOD is still subject to the same economic pressures that all transactional entertainment is subject to. In difficult economic circumstances, when expendable income is squeezed, consumers have demonstrated gravitation towards subscription business models for video consumption.

TV-based TVOD movie transactions have also declined in the southern European countries, which have seen continued economic strife in the form of high youth unemployment and stagnating wages. In Italy, movie transactions decline by an average of 2% every year between 2009 and 2013 and declined by an average of 14% every year in Spain.

Germany is relatively stronger economically, but has been perpetually under-developed relative to its market size; the result of a lack of investment which has left fragmented infrastructure between local television providers and German homes in large areas of the country. Only 2,915 German households were VOD-enabled in 2013, compared to neighbouring Belgium with 3,226 and the Netherlands at 4,820 VOD enabled households. However, this is forecast to improve, as Germany will surpass these two much smaller markets during the forecast period, increasing to 7,386 VOD homes by 2017, with the continued digitization of cable playing its contributing role in driving the roll-out of VOD capabilities.

Less mature movie regions have seen strong growth for TV-based VOD consumption, but again this growth is uneven across regions. TV-based VOD movie transactions in Central and Eastern Europe increased by an average of 58% each year between 2009 and 2013 - to reach 31.1 million. However, Poland accounts for a significant proportion of these total transactions relative to its market size (45% in 2013). Russia also accounted for a 45% share of regional TV-based VOD transactions, but this is generated from an installed base of 34.6 million pay TV households compared to Poland?s 12.2 million.

In 2013, 41% of TV households in Poland were VOD or nVOD enabled; when push-VOD homes are included, total household penetration ?increases to 46% - an increase from 3.1% of households in 2008. Russia had 3.4m VOD-enabled households compared to Poland at 1.9m in 2013, however, this only accounts for a penetration rate of 6.4% of Russian TV households. However, 20% of Russia households have access to push-VOD in 2013.

The growth in TV-based TVOD movie consumption in the majority of developing markets is very much related to both growth in the installed base of on-demand households and their relative penetration of total TV households - with new adopters tending to have higher buy rates.

However, the comparison between Poland and Russia illustrates that in terms of driving consumption, not all VOD platforms are created equal. Also important is how on-demand capability enters into the home. If a household is equipped for IP-VOD there is a necessity to actively connect a standalone set-top box (STB), as opposed to other scenarios, were households may become VOD-enabled by default.

Of the 743 million pay TV households worldwide in 2013, Asia Pacific accounted for 58%. Asia Pacific is a region of extremes, ranging from highly developed countries with high average prices and sophisticated retail and logistical infrastructure (e.g. Japan and Australia) to those like China and India - with vast populations - where average incomes are substantially lower and infrastructure is still developing. As a result, vast areas of the region cannot technically support VOD platforms.

The Asia Pacific countries covered by this analysis have a combined population of 2.9 billion people, but only generated 279.5 million TVOD movie transactions in 2013, in comparison, North America generated 358.5 million transactions from a population of only 359.1 million.

However, one country where TV VOD movie consumption has seen very strong growth is South Korea. In 2009, South Koreans rented 85.1 million movies via TV-based VOD platforms, increasing to 111.9 million by 2013 - forecast to increase further to 164.3 million movie transactions by 2017. This is in comparison to Australia, which will only generate 8.3 million TV-based movie transaction in 2017 and Japan, which will generate 38.6 million, despite having over double the size of TV households (52,466 to South Korea's 18,533, forecast for 2017).

Driving this growth is the explosion of VOD-enabled households in South Korea, which will reach a penetration rate of over 100% by year end 2014 - as a proportion of homes begin to receive multiple VOD services. In comparison, Japan will only have a VOD household penetration rate of 17% by year end 2014, increasing to 25% when nVOD homes are also accounted for.

Latin America as a region has also seen strong growth for TV-based VOD, increasing from just 8.4 million movie transactions in 2009 to 28.6 million in 2013. The number of households which have access to VOD has increased by an average of 61% every year between 2009 and 2013, with the number of nVOD homes ?increasing by 21%.

By 2017, Brazil will account for 60% of VOD households in the region, impressive as the platform has only been available to Brazilian consumers since 2011. As a result of its launch total TV-based VOD movie transactions in Brazil increased by 55% between 2010 and 2011, and are forecast to increase to 21.9 million by year end 2014. This means the volume of TV-based VOD consumption in Brazil will be comparable in size to both Russia and Germany by that time.

However, important to note is that VOD homes in Brazil are constricted to heavily urban (in the south of the country) areas where enough infrastructure has been invested in. The north, which consists of vast tracks of the Amazon jungle, is largely serviced by satellite nVOD.

Both Latin America and Central and Eastern Europe show very strong growth, but still lag behind the other three regions in terms of on-demand-enabled homes. In the case of Asia-Pacific, despite having the largest installed base of VOD/nVOD-enabled homes worldwide, it still underperforms relative to its size as an entire region in terms of consumption.

In all three cases, each region has one country which stands out as further advanced than its direct neighbours, which very much drives total growth for TV-based VOD consumption for the region as a whole. For all its advantages as a movie distribution platform, the vast geographic challenges and huge economic disparities between and within countries, have so far acted as, limiting factors for the growth of the platform worldwide.

TANIA LOEFFLER joined IHS in late 2009, first as a Research Analyst for the Broadband Media Team, where she tracked the international online movies market and content for connected devices, before transitioning to the Video Team. Prior to IHS, Tania worked in Toronto, Los Angeles and London in various roles in film, television and digital media. Contact: www.ihs.com.

This is one of several editorial features included in the DVD and Beyond 2015 magazine. Ask for your free copy.

Story filed 03.05.15

More Articles...