Europe's online source of news, data & analysis for professionals involved in packaged media and new delivery technologies

ANALYSIS: Transactional movies - the big picture; global spending hits $62bn

After a four-year period of declines and slowed growth between 2008 and 2011 (CAGR -0.2%), total worldwide consumer spending on transactional movies recovered in 2012 to reach $62.4bn, surpassing the $61.5bn total for movie spending in 2008. Furthermore, consumer spending on transactional movies, which are defined as movies paid-for at the point of consumption, is forecast to continue to grow by a CAGR of 2.6% between 2012 and 2016. TANIA LOEFFLER, Video Research Analyst at IHS Screen Digest examines the data.

Asia-Pacific leads the way

Overall, worldwide growth in 2012 was largely generated by consumers in Asia Pacific. Consumer spending on transactional movies in the region increased year-on-year by 4.6% to reach $15.8bn in 2012. Asia Pacific currently commands a 25.3% share of worldwide movie spending and this share is forecast to increase to 28.2% by 2016. Asia Pacific is poised to overtake Western Europe as the second largest region for consumer spending on movies by year-end 2013. It is important to note, however, that a significantly higher proportion of locally-produced movie content is consumed in Asia Pacific in comparison to Western Europe, especially in countries such as India and China.

In 2012, consumers in Asia Pacific spent $10bn on going to the cinema, representing an11.9% increase over 2011. In combination with the popularity of higher-priced 3D and digital theatrical content across the region, new cinema construction in China has been driving rapid growth for theatrical transactions. Cinema admissions in China increased year-on-year by 16.2% to reach 482m in 2012 and consumer spending on movies consumed in theatres increased by 31.9% to reach $2.7bn over the same time period. This growth increased China's share of total theatrical spending in Asia Pacific, from 22.7% in 2011 to 26.8% in 2012 (forecast to increase further to a 30.6% share in 2013).

Consumer spending on movies increased significantly in other regions. By 16.7% in Central and Eastern Europe to reach $2.2bn and by 6.6% in Latin America to reach $2.7bn; but ultimately these markets still remain very small, with only an 7.8% combined share of worldwide movie spending in 2012.

As in Asia Pacific, much of the growth in movie spending in these developing markets is driven by theatrical movies. In Central and Eastern Europe, consumer spending on cinema tickets increased by 20.8% over 2011 and accounted for an 84% share of total consumer spending on transactional movies in the region. Latin America echoes this with theatrical spending increasing year-on-year by 10.3%, capturing a 67.4% share of total transactional movie spending in 2012.

The modernization of existing cinemas and the construction of new modern multiplexes in all three of these regions is driving the digitization of cinema projectors - allowing for a generally improved movie-going experience and higher priced 3D content - which both increases transactions and pushes the average price of a cinema ticket upwards. What also may account for theatrical's ability to dominate growth and share of consumer spending in these regions is that the theatrical experience cannot be directly pirated, and thus is more able to capture legitimate spending than other movie delivery channels.

In contrast, total growth for the two most mature movie markets, North America and Western Europe, has been muted. Declines in spending on physical media (DVDs and Blu-ray Discs) pulled down the total for movie spending in 2012, even as consumers in both regions increased their year-on-year spending for movies consumed on digital platforms and in cinemas.

Consumer spending on transactional movies in Western Europe was stable at $16.1bn, a -0.4% decline over 2011. The Sovereign Debt crisis has created both fluctuations in the value of the Euro and, amongst other factors, diminished consumer demand for movies purchased on physical media. Physical purchase, declined to $4.5bn in 2012 down from $4.9bn in 2011 (a year-on-year decline of 9.4%). Spending on DVDs and Blu-rays in Western Europe is forecast to decline further, by a CAGR of 11.5% between 2012 and 2016; from a 27.7% share of total transactional movie spending in the region to a 16.8% share during the same time period.

North Americans still spend the most on transactional movies by far (approximately $80 per capita per year), accounting for a 41.7% share of worldwide movie spending in 2012. This is forecast to remain at a stable 39.4% share through to 2016. The total for consumer spending on movies in North America increased by 0.8% to reach $25.6bn in 2012, however, total movie transactions declined by 3.4%, from 4.3bn in 2011 down to 4.1bn in 2012.

Movie purchases made online in North America increased year-on-year by 36.6% to reach 29.2m transactions. The rental of movies online also increased, to 112m transactions, an increase of 57.3% over 2011. Despite this strong growth, movies purchased or rented via over-the-top (OTT) online movie services still only accounted for a combined $836m, or 3.3% of total consumer spending on movies in North America.

Theatrical is the key driver of consumer spending growth worldwide

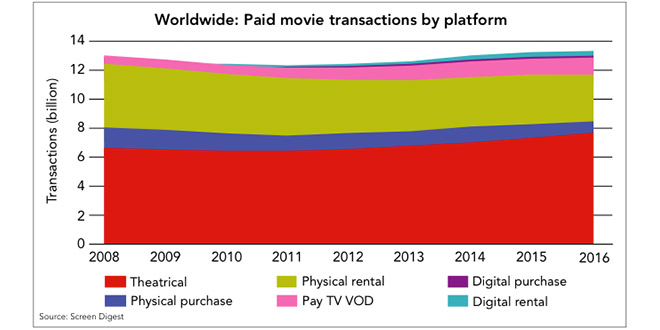

Worldwide, consumer spending on theatrical grew 6.6% to reach $33.4bn in 2012. Across all 5 territories, consumers overwhelmingly demonstrated that the cinema experience remains the most desirable way to consume movies, with theatrical accounting for 53.2% of total movie transactions.

Despite changes ahead for movie distribution platforms in the home (decline in transactions for movies on physical discs and growth for movies consumed via digital platforms) theatrical will continue to dominate transactional movie consumption worldwide. Movies consumed in the cinema will account for an even larger 58.4% share of total transactions by 2016 and will drive the overall growth for consumer spending on movies worldwide between 2013 and 2016. Consumer spending on theatrical content is forecast to increase by a CAGR of 6.0% to reach $42.1bn by 2016.

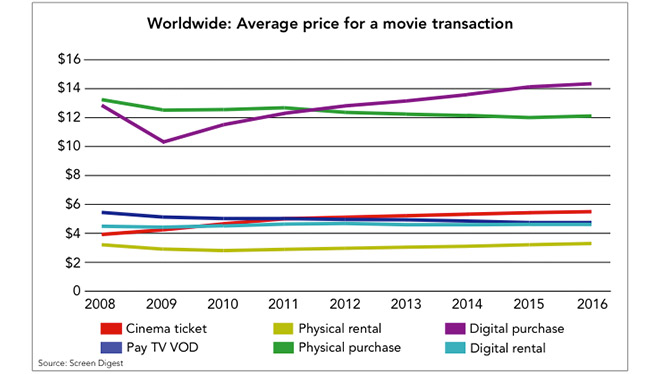

Even in the mature theatrical markets of North America and Western Europe, theatrical will generate increased consumer spending, without a significant number of new theatrical transactions being generated. This is the result of the continuous increase in the average price of a movie ticket, which typically increases in line with general inflation, across all five regions. Average price for a cinema transaction worldwide increased from $4.92 in 2011 to $5.09 in 2012 (a year-on-year increase of 3.4%) and is forecast to increase by a CAGR 1.9% between 2012 and 2016. Higher-priced 3D content has also made a significant impact in increasing average price worldwide, but it will have less impact through the forecast period as an already established and persistent part of the cinema experience.

Unlike theatrical, physical media is subject to the more aggressive competition on price inherent to many retail environments. At the same time, the opportunities for consumers to access movies have become increasingly diverse and physical discs must now compete with digital and pay TV platforms for consumer attention in the home.

Consumption and consumer spending on movies, either purchased or rented on physical discs continued to decline, from $24.8bn in 2011 to $24.1bn in 2012 (representing a -2.8% drop). Worldwide decline is forecast to continue for both DVD and Blu-ray Disc purchases and rentals, however, despite this, physical will still account for a combined 30.9% of total worldwide movie transactions in 2016.

As both business models for physical consumption decline, physical rental is set to overtake physical purchase as the second largest generator of worldwide consumer spending on transactional movies. This dynamic helps to drive consumer spending decline, as the average price of a physical rental transaction at $2.93 in 2012, is much lower than the average price paid to purchase a movie on a physical disc ($12.32). Physical purchase transactions are forecast to decline worldwide from 1.1bn in 2012 to 781m by 2016 (a CAGR of -7.8%) with average price for a physical disc forecast to fall by a further CAGR of 0.6 per cent between 2012 and 2016.

The decline in higher value physical purchase transactions will result in physical media struggling to maintain share of worldwide movie spending. Physical media, retail and rental combined, is forecast to lose an approximate 10% share of total worldwide consumer spending, from 38.9% in 2012 down to a 28.7% share by 2016.

The digital future belongs to rental

The preference for physical rental as a consumer behavior is translating into the digital space, even in regions like Western Europe, where physical purchase has traditionally dominated physical video transactions. TV-based Video-on-Demand (VOD) and digital rentals from over-the-top (OTT) services such as Apple's iTunes vastly outpaced the number of movies purchased online in 2012. Pay TV VOD transactions increased by 15.9% in 2012 to reach 685m and digital rental increased by 61.5% year-on-year to reach 174m. In contrast, digital purchase transactions increased to only 52m, from 39m in 2011.

Average price for a digital purchase increased year-on-year by 4.6% to reach $12.88 in 2012. Prior to 2010 the average price paid to purchase a movie online echoed average price for a physical purchase, with average digital price benchmarked below the average price of a new release physical disc. This trend is now diverging, with average digital price forecast to surpass physical, to become the most expensive distribution platform worldwide during the forecast period (2012 to 2016).

This trend is not reflective of the increase in demand for digital retail movies, but the result of a number of factors. The legitimate consumption of transactional movies over the internet is largely limited to North America and Western Europe, and some key markets such as Australia and Japan, where average prices are much higher for all movie distribution platforms in comparison to most developing markets. In addition, average price for physical purchase is comprised of lower-priced catalogue and premium-priced new release transactions; digital offerings are heavily focused on new release titles. This, in combination with growth in consumption for more expensive high definition (HD) content, is pushing average price for the purchase of an OTT movie upwards.

Movie purchasing online has not developed into an exciting enough consumer proposition to drive the level of worldwide legitimate consumption needed to replace the decline in physical retail transactions. The three-major device-based online movie services (iTunes, Sony, Microsoft), which are the only market players to drive measurable consumption to date, have expanded their global reach, but have yet to provide services in some of the world's most populous markets, such as China and India.

Pay TV TVOD movie spending increased year-on-year by 15.1% in 2012 to reach $3.4bn worldwide, forecast to increase by an average of 9.4% every year during the forecast period to reach $4.9bn by 2016. The vast majority of this growth in consumer spending on TV-based VOD will be coming from North America and Western Europe, which combined accounted for 63.6% of the growth in transactional movie spending on pay TV VOD platforms in 2012.

At 431.6m, Asia Pacific accounts for the majority of pay TV homes globally by a significant margin, however, much of the cable and satellite infrastructure across Asia Pacific (with the exception of Australia and New Zealand) still struggles to technically support VOD. As a result the region only accounted for 14% share of the total for worldwide consumer spending on TV-based VOD movies in 2012, forecast to increase only to a 17% share by 2016.

Total consumer spending on buying and renting movies digitally increased to $4.9bn in 2012. Although consumer spending on digital movies continues to be strong, combined spending on all three digital platforms in 2012 reached only a 7.8% share of total worldwide movie spending. Various limitations continue to mute the potential of legitimate consumption and thus transactional spending on digital movies worldwide. As a result, consumer spending on digital movies - on TV-based VOD and OTT rental and retail services - is forecast to increase to only a 10.7% share of worldwide transactional movie spending by 2016.

TANIA LOEFFLER joined IHS Screen Digest in late 2009, first as a Research Analyst for the Broadband Media Team, where she tracked the international online movies market and content relationships for connected devices, before transitioning to the Video Team in May 2011. Prior to IHS Screen Digest, Tania worked in Toronto, Los Angeles and London in various roles in film, television and digital media and she brings an extensive understanding of these sectors to her coverage of the home entertainment industry. Tania has a BA (Honours) in Film, Culture and Communication from Queen's University, Canada, and an MA in Communication Management from the University of Southern California. Contact: www.screendigest.com.

This is one of many in-depth features included in the forthcoming DVD and Beyond 2013 magazine. Reserve your free copy.

Story filed 15.09.13

More Articles...