Europe's online source of news, data & analysis for professionals involved in packaged media and new delivery technologies

ANALYSIS: The future of video is here - Europe's 'hybrid consumers'

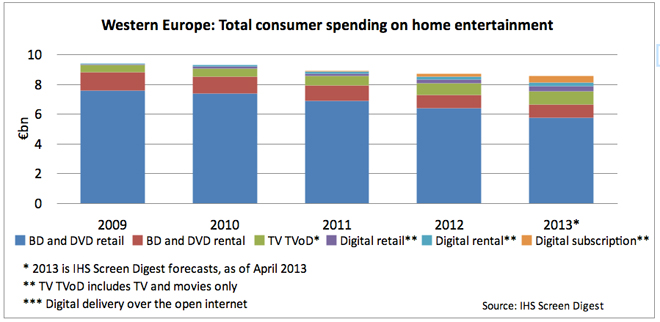

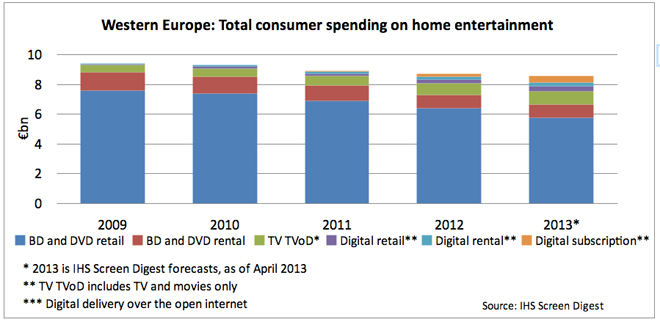

Europeans have become 'hybrid consumers,' enjoying films across multiple formats and platforms, says TONY GUNNARSSON, Senior Analyst at IHS Screen Digest. Last year, consumers in Western Europe spent a massive €9.11bn watching movies on both disc-based and digital platforms, a fall of just 1.6% on 2011's revenue.

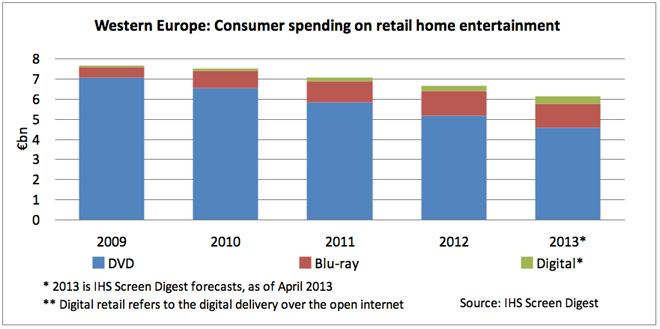

Although spending on physical media continued to fall, down 7.8% to a total value of €7.31bn, packaged media remained by far the largest area of consumer spending on video content, representing 80.2% of total European video market. The DVD may have been prematurely consigned to the history books by some observers but, with Europeans spending €5.95bn on the format in 2012, it is clear that the 'old and trusted' standard definition format continues to be European consumer's number one video format.

It is, of course, correct to note that DVD consumption is falling - the number of DVDs bought in Europe last year dropped 12.7% to a total of 466.4 million units - but no other video format (or online delivery method) has so far proven as popular on a mass-market scale in Europe. Although the DVD format is in decline at no point in the near future will DVDs disappear from retail or rental store shelves. DVD's successor, the Blu-ray Disc continues to be talked about in negative tones by some observers but it is already established as a significant format in Europe. Revenue was up 18.5% in 2012 as Europeans spent €1.38bn buying and renting physical hi-def video.

The European market for BD today is larger than that for transactional TV VOD and indeed, when viewed as a separate component, bigger than all the internet-based digital video delivery platforms combined. Digital consumption, which often includes video content consumed over the open internet and via Pay TV on-demand services, is the fastest growing area of video consumption when all platforms are combined. This is the reason why digital video continues to be the hot topic both among consumers and the industry alike. Last year, overall digital movie consumption grew to €1.80bn in Europe, an increase of 34.8% on 2011.

Within that grouping, Pay TV transactional video-on-demand (TV TVOD) continues to be the largest area of consumer spending, at €1.06bn, up by +14.3% in 2012. This firmly places TV TVOD as the second largest area of European video overall, second only to physical video, accounting for 11.7% of European spending video last year. Digital subscription, however, is growing the fastest, having more than doubled in size to €262.4m in 2012. This remarkable growth is due to the launch by US online rent-by-mail and streaming pioneer Netflix of services in the UK, Ireland, Sweden, Norway and Denmark in late 2011 and during 2012.

Netflix is not the first or the largest provider of video streaming by subscription services in Europe but the first year uptake of its services by European consumers reveals the power of big US brand names among Europeans. The digital video subscription sector has now overtaken digital rental, which last year was valued at €201.0m, and will soon also overtake digital retail, also known as electronic sell-through (EST), which at €270.8m was still the largest area of internet-based video in 2012.

In 2012, the key narrative for home video was yet again that of a falling DVD market. It seems that for some observers the transition to an entirely digital video market can't come too soon but, away from the hype, the sheer scale of DVD consumption means that, even in decline, the format is still going to be important throughout our forecast period and beyond.

European consumers are confidently navigating through the many video platforms where they can access paid-for movies, be it DVDs and BDs, digital video and TV VOD. Video consumption appears to be already shared between multiple devices, formats and platforms. It seems likely that there is no such thing as a consumer that only watches movies on one platform, what happened in 2012 is that even more of us have become hybrid consumers that pay to view movies on a multiple of services and formats.

Video specialists threatened

At the same time, economic uncertainties in a number of European markets and slow growth in others have impacted on the video market; indeed, such economic pressures are partly speeding up the transition from physical to digital video consumption. In a declining, disc-based entertainment environment, video and music retailers and rental outlets across Europe are finding it tougher to continue trading. There are, of course, still plenty of consumers who buy and rent video discs but the loss of consumer spending in real terms has forced some retailers to close and others to shift self space to more profitable categories.

While some disc sales - particularly destination purchases such as new release - are picked up by competitors, consumers are being presented with physical discs for purchase less frequently and with less range depth, making it harder for them to pick-up video on impulse. This forces consumers to look for alternatives places to access video products and, more often than not, this will be an online retailer of physical goods such as Amazon or an online shop for digital video like iTunes.

While the UK has already lost much of its once unrivalled specialist retail market, the remaining specialist stores continued to see lower sales volumes though 2012. The UK's last remaining high street video and music chain HMV's first began to report troubles back in 2011 when it survived debt problems. In January 2013, both HMV and Blockbuster UK, the UK rental store market leader, went into administration. While both companies have since been acquired by restructuring specialists Hilco and Gordon Brothers respectively, UK high-street difficulties echoed a number of other video retailer closures across Europe.

Virgin megastores in France also declared insolvency in January 2013, which will result in the closure of its 26 stores in France. This coincided with an announcement from fellow French retailer FNAC that it will sell its Italian retail operation. In Germany, the retail giant Media-Saturn Group has been quietly restructuring its management of the two bricks-and-mortar brands with a view of building a unified

e-commerce platform.

IHS Screen Digest analysis indicates that the changing video retail environment across Europe - as opposed to wholesale shifts in consumer habits away from disc-based consumption - is largely the reason why physical video consumption is falling overall. Many European consumers still want to be able to watch movies on discs but simply find it harder to find outlets to buy or rent video.

Big five Euro markets

Across Europe, individual markets increasingly demonstrate differing trends in terms of video consumption. Previously, the UK, Germany, France, Italy and Spain were billed as the 'Big Five Euro markets' but the latter two countries? economies have suffered more in recent years and now the Nordics and Benelux regions place fourth and fifth respectively in European video market rankings. The UK continues to be the largest European video market, accounting for a third of all consumer spending on video in Europe. In 2012 the UK market grew by 2.6% to €2.78bn. This growth was partly due to increases in digital video consumption (up 47.5% overall).

Spending on buying and renting DVD and BD dropped by 4.6% overall to €2.22bn, despite modest growth in video rental (up 1.2%) where some consumers opted to rent BDs instead of DVDs, which compensated for a fall in spending on DVD rental. Digital video and TV TVOD now generate a fifth of the UK video spending at €558.7m. In the UK consumers now spend more on digital video (€310.4m) than on TV TVOD (€248.3m) as a result of massive growth (+308%) in digital subscription in the wake of Netflix's launch in the UK with continued growth for incumbent rent-by-mail operator Lovefilm?s streaming services.

The European success story of recent years and in 2012 is the German market; it experienced a stable year in terms of consumer spending on total video, ending the year flat at €1.77bn despite physical video tipping into an annual decline (-4.4% ) for the first time since 2006.

The decline was compensated for by growth in digital video and TV TVOD though it remains a proportionately small part of the German market, generating just one tenth of the market compared to one fifth in the UK. The German digital video market is still developing and to date the market has not benefitted from a strong digital subscription operator such as Netflix. Nevertheless, last year Germany increased its proportion of the European video market generating almost 22% of total European spending on video.

Once the second largest market, the French video market has dropped to third place and experienced an overall decline in 2012. Driven by a steep decline in physical video consumption, which fell 11.9% to €1.11bn, French consumer spending on total video dropped 4.8% overall to €1.55bn. For the second year in a row, French consumer spending on buying DVDs and BDs dropped by about 10%, and spending on renting DVDs and BDs again dropped by more than 20% for the seventh consecutive year. French digital video, delivered via the open internet, mirrors that in Germany with an overall consumption of movies on digital platforms accounting for 7.3% of total video (Germany 7.1%).

Also like Germany, no digital subscription services have launched in France to date. However, thanks to the country's well developed TV TVOD market, France benefited from being the largest overall digital video market in Europe, with such transactions accounting for a fourth of its market.

Beyond the big three Euro markets, the Nordic and the Benelux markets, which account for 11.6% and 6.3% of total video spending in Europe respectively, experienced stability (Nordic +0.2%, Benelux -0.3%). Italy and Spain, which today account for less than 3% of European video market each, experienced steep declines of 12% and 20% respectively.

New Products enriching consumer experience of video

Having been around since 2010, Blu-ray Disc 3D (BD3D) may not be seen as a new format anymore but, with consumer adoption lagging the US by more than a year, the hi-def 3D format is only now starting to come into its own in Europe. Building on the success of 3D movies in theatres, BD3D is the industry's official home video 3D format, and the only 3D in-the-home offering to enable the full 1080p hi-def 3D experience.

BD3D seems to have been so far ignored by the media, perhaps because viewers require not only a 3D TV but a 3D BD player and 3D glasses as well as a BD3D disc in order to view a 3D movie in the home. It has not been shunned, however, by the intended target group of tech-savvy early adopters and serious film fans. With more than 200 titles available on the format in Europe in 2012, a small group of 7.3 million BD3D-equipped households in Europe spent €87m purchasing around 5m BD3D discs, representing nearly 8% of the total European BD market.

Additionally, there is the prospect of the home video industry's latest digital initiative to come. UltraViolet is a cloud-based digital locker solution that allows consumers to build a film collection in the cloud and greater level of convergence when it comes to purchased video products. In 2012, UV had launched only in the UK and Ireland within Europe. IHS Screen Digest research indicates that in the UK, 90 titles containing UV redemption codes had been released in 2012 on DVD and BD, from nine studios.

Tony Gunnarsson is a senior analyst in IHS Screen Digest's Video team where he tracks and analyses developments in the physical video sector, with expertise in DVD and Blu-ray Disc markets, Blu-ray 3D, UltraViolet and online rent-by-mail services. Contact: www.screendigest.com

Story filed 15.05.13

More Articles...